Over the past 30 years of China's LED industry development, the government has formulated and implemented the “863†plan green lighting project, semiconductor lighting project, “Ten Cities and Ten Thousand†semiconductor lighting application demonstration project pilot and other policies, and vigorously support the development of LED industry, has been preliminary Form a relatively complete industrial chain, and have certain advantages in the downstream. At present, there are more than 3,000 companies in the domestic semiconductor lighting industry, including 62 out-of-band chip companies, about 600 packaging companies, and more than 2,000 application companies. In 2011, China's optoelectronic semiconductor lighting industry reached 156 billion yuan. In general, China's LED industry is accelerating, and it has become the world's largest LED outdoor lighting market. It has also become the world's largest producer and exporter of LED applications, and the LED industry is on the rise.

Technology management includes the planning, development and execution of technological capabilities to plan and complete organizational operations and strategic objectives, and is of great importance to the sustainable development of the LED industry. However, China's current technology management system seriously restricts the development of the LED industry. First, the science and technology management system does not meet the requirements of the market economy. The contribution rate of technological progress to economic growth is less than 30%, and high-tech accounts for less than 10% of economic growth. Secondly, the independent innovation capability of enterprises is weak, and most of the researchers are in universities, research institutes, etc., not enterprises. Thirdly, the internal structure of science and technology management is unreasonable, the establishment of independent scientific research institutions and the difficulty of the flow of scientific and technical personnel.

I. Analysis of the status quo and problems of technology management in LED industry

1. Industry lacks technology strategy

The development status of China's LED industry can be described as everywhere. In addition to 13 national-level industrialization bases, many provinces and cities have set up their own semiconductor lighting bases. Lack of coordination and cooperation among regions has resulted in the lack of effective allocation of industrial resources, resulting in a disordered layout of the LED industry and a vicious regional competition. Individual governments have also experienced problems such as local protectionism and low-level redundant construction. Due to the low barriers to entry and entry of LEDs in the middle and lower reaches of the LED industry, the industrial structure of leading enterprises with a large number and small scale and lack of leading industrial development makes the company lack of R&D investment, low product quality and lack of concentration of enterprises, resulting in lack of market competitiveness. . At the same time, traditional lighting companies, state-owned capital and private capital have entered the LED industry one after another. Most of the products are copied and imitated by each other. The homogenization competition causes price wars, and the industry lacks scientific decision-making and reasonable planning.

At present, China's LED application demonstration project has formed a certain scale, but most of them are government projects; in terms of capital investment, most of the application demonstration projects are direct investment by governments at all levels, or investment by undertaking engineering units, while commercial banks and investment There is not much use of private funds such as funds and corporate funds. Such a single promotion and application model is prone to problems such as overcapacity and needs to be addressed.

2. Industry lacks technological development

The key equipment of China's LED industry is heavily dependent on foreign imports. Whether it is upstream MOCVD or mid-stream chip packaging and test equipment, it is mainly imported from abroad. Chip, epitaxial and high-power LED packages are the core technologies of LEDs, and most of these extremely important core technologies are patented by Japan Nichia, Cree, Toyoda Gosei, etc. The international LED giants are in control, and the patents applied by Chinese enterprises are mainly concentrated on the periphery and relatively weak. The patents for the phosphors YAG:Ce and YAG:Tb for white LED packaging are also monopolized by Nichia and Osram respectively. In order to meet the short-term demand in the domestic market, most domestic packaging companies mainly produce chip LEDs, in-line LEDs and TOP LED devices with low technical content. However, due to the absence of core patents, products will be subject to patent restrictions and obstacles when exported to foreign markets. . According to statistics, among the 222,000 LED street lights and tunnel lights installed in the “Ten Cities and Ten Thousand Miles†pilot activities, almost all of the lighting manufacturers use imported chips, Cree (40%), Lunileds (20%), Osram (16). %), Nichia (10%) and so on occupy nearly 90% of the market, and the remaining 10% of the market is mostly divided by Korean companies and Taiwanese companies. The market share of domestic chip companies is almost zero.

At present, China's research and development in the field of semiconductor lighting is seriously inadequate and its power is scattered. For example, Philips' 1 year R&D investment cost is 44 million Euros, which is equivalent to the sum of the five years of major projects of China's “863†and “Semiconductor Lighting Projectâ€. China's LED enterprises and independent R&D institutions are sparsely invested and have weak R&D capabilities, especially the lack of open technology research and development. In China's semiconductor lighting industry, core equipment such as MOCVD must rely on imports. Although upstream epitaxial materials and core devices have already achieved mass production, they are still at the low-end and low-end, low-cost, high-reliability core devices. Although midstream packaging and downstream integration applications have formed mass production and accelerated development, there is still a lack of research and application integration technology for innovative applications. What Chinese companies are lacking is low-cost, alternative, and standardized LED products.

3. The industry lacks a standard system for scientific and technological management

China's LED industry standard certification system lacks overall planning. At present, China has formulated 12 national standards and 10 lines of standards, but most of them are definitions, terms, safety requirements, test methods and other standards, which are not compatible with existing application design standards. Due to the rapid development of LED technology, the development of the national standard takes a long time, and the newly released standard has lagged behind the needs of the industry. These standard systems are basically based on international standards and European and American standards. Without the corresponding independent research work, it is difficult to provide practical technical support for the standards. At the same time, due to the lack of overall layout and unified planning for the development of standards and the construction of inspection platforms in various provinces and cities, there is a big difference between local standards in a place, and LED companies are also helpless. Therefore, as long as domestic standards have not yet formed a systematic system, the chaotic situation of industry standards cannot be changed.

In addition, China's LED standard testing has a multi-head management phenomenon. The regulatory bodies involved in LED standards include the “Industrial and Information Industry Department Semiconductor Lighting Technology Standard Working Groupâ€, the “National Lighting Appliance Standardization Technical Committeeâ€, and the “Industrial and Information Industry Department Flat Panel Displayâ€. Technical Standards Working Group" and so on. This kind of multi-head management, the overall coordination is poor, lack of overall planning, affecting the long-term development of the LED industry. LED technology is an interdisciplinary, cross-disciplinary, and cross-industry technology, but there is a lack of communication and coordination among management agencies, resulting in inconsistent and unmatched industry standards. At the same time, the testing methods and standards of domestic testing institutions are not uniform, the testing capabilities are uneven, and the data derived from each testing laboratory is inconsistent. As a result, mutual recognition difficulties are caused, which also hinders the export of domestic products. The lack of a standard system for technology management is indeed a big stumbling block in the development of the LED industry, and it is urgent to change.

4. The industry lacks leading talents in science and technology management

In the United States, researchers within the company account for about 80% of the total number of researchers in the country, and research and development costs in enterprises account for about 65% of the total national cost. The application research in China's enterprises only accounts for about 10% of the national total. Most researchers are quietly doing R&D work in research institutes and research institutes independent of enterprises. Because it is difficult for science and technology personnel to flow, it is difficult to enter enterprises and markets, leading to the departure of market demand for LED technology development research in China, and the weak independent innovation capability of enterprises. In this way, the LED industry has limited capacity for sustainable development.

Researchers within the company, mainly through the introduction of research and development teams from Taiwan, gradually established and cultivated their own research and development team. In this way, the general R&D talents have accumulated in quantity. At present, the general research and development of LED in the middle and lower reaches has little problem. However, LED devices must have a qualitative breakthrough. To gain an advantage in the upstream, there is still a need for leading talents who can lead enterprises to carry out technical research. At present, there are very few senior technology R&D talents, senior design talents, corporate executive talents, and senior test talents in the LED industry, which are not conducive to the upgrading of China's LED industry.

Second, the recommendations for LED industry development and technology management

1. Develop detailed industrial development plans

In view of the strategic position of emerging industries, the development of LED industry must have a global vision and a strategic vision. It is necessary to pay special attention to the layout before industrialization and the formulation of intellectual property strategies, and to find a market-oriented combination of production, education and research. Among them, it is necessary to adjust and upgrade the industrial structure, break the traditional development model and outdated thinking, and strengthen the cultivation of high-tech research and development capabilities to steadily enhance the comprehensive competitiveness of China's LED industry development. The United States, Japan, South Korea and other advanced countries in the LED industry have developed relatively similar LED plans. China can learn from the experience of the above countries and develop LED industry development plans with Chinese characteristics and LED industry development road maps. The development plan should be a comprehensive R&D and industrialization plan including capital, operation, project, evaluation, etc., covering basic technology research, core technology research, standard development, product development, commercialization needs, and feasibility evaluation of inter-industry cooperation. aspect.

2. Improve the level and ability of technology management

Focusing on the major needs of LED industry development, we will integrate domestic and foreign scientific and technological innovation resources, strengthen cutting-edge technology research, and support enterprises to strengthen the domestic and international layout of intellectual property rights. Strengthen the construction of technological innovation capability of enterprises, guide and encourage enterprises to increase investment in research and development, promote the gathering of innovative elements of enterprises, conduct research on cutting-edge LED lighting technology, and seize the commanding heights of the next generation of white light core technology. Support enterprises to build national research centers, engineering laboratories, key laboratories, enterprise technology centers and other innovative platforms to ensure the sustainable development of China's semiconductor lighting industry. Support the application and application of intellectual property, strengthen knowledge

The management and protection of property rights, improve the intellectual property law system, and crack down on illegal and infringing behavior. Explore the establishment of a combination of technology, patents and standards, accelerate the transformation of intellectual property, promote the patentization of core technologies, and standardize patents. At the same time, deepen the cooperation between industry, university and research institutes, improve the long-term mechanism for sending science and technology commissioners in enterprises, and implement the action plan for the combination of production, education and research. Strengthen the cooperation planning and guarantee system construction of industry, university and research. Focusing on key areas of the LED industry, we will organize and implement a number of major projects of industry-university-research cooperation, and support universities and research institutes to jointly undertake major national science and technology plans and industrialization projects.

3. Establish a development system that adapts to science and technology management

The core patents of LED technology in the world are basically controlled by several foreign companies. The United States and Japan have formed a patent network for the LED industry. Although China's LED has a certain number of patents, most of them belong to peripheral technologies. As of August 2010, the number of patent applications related to the original LED industry in China was more than 25,000, and the number of patents related to global LED lighting was more than 124,000. Among them, the number of original patent applications in Japan was more than 49,000, accounting for the global total. Nearly 40%; the number of original patent applications in China is more than 25,000. At the same time, due to the lack of original science and technology, it is difficult to break through foreign patent barriers. At present, it is possible to integrate the national LED industrialization base and the research and development resources of relevant universities and research institutes, establish and improve the LED patent database system, closely follow the world LED patent technology frontier, form an open platform, from the overall industrial layout and technology development layout. Track and fill technical vacancies; use the network platform as a link to integrate local IP offices, assist and support universities, enterprises and related associations to work together on LED patent databases; set up a database management center to guide enterprises to conduct LED patent Internet of Things Construction, regularly publish real-time information on LED enterprise sector patents, cultivate patent early warning capabilities, improve the ability to create, use and protect intellectual property rights, thus avoiding patent barriers of foreign companies and avoiding the “patent trap†of major international LED companies.

At the same time, China should strengthen the strategic research on LED standards, take the existing standards of LED industry as the guidance, implement the requirements of national LED lighting standards, and establish a scientific and perfect LED standard system. For those products that are not mature in technology, we should study and formulate technical specifications with guiding significance as soon as possible, and improve the application standard system and installation technical specifications. For LED lighting products with relatively mature technology and basic product stereotypes, safety, energy efficiency and performance should be gradually established. And other aspects of the certification evaluation system.

Source: Eastern Securities Research Institute.

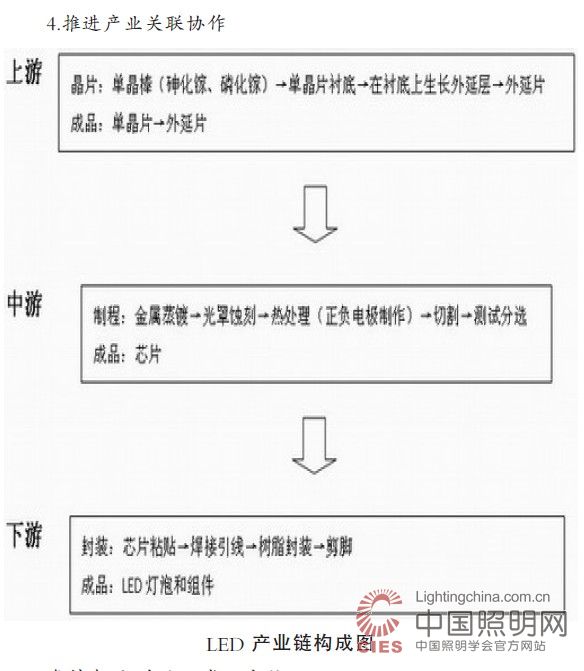

From the analysis of the LED industry chain, the four major gathering areas of China's LED industry have scale advantages and industrial supporting advantages. At the same time, there are domestic best scientific research resources and abundant funds in the industrial agglomeration area. Therefore, these resources should be fully revitalized, relying on advantageous industrial clusters, planning and constructing a number of industrial advantages, industrial support, leading enterprises, innovation The LED industry cluster with outstanding capabilities will guide funds, technology and talents to gather in the industrial bases to form industrial clusters with concentrated factors, concentrated scale and complete facilities. At the same time, through the construction of industrial agglomeration areas to promote industrial space agglomeration, through the construction of professional service system to improve the industrial agglomeration environment, guide the strategic emerging industry resources to accelerate the centralized concentration, form a group of unique emerging industrial clusters and industrial bases, forming a more The strategically emerging industrial clusters with strong competitiveness will drive the sustained, rapid and healthy development of the regional economy.

5. Emphasis on training and introducing talents

Starting from the actual demand of China's LED industry for high-end talents, we will continue to improve talent incentives and supporting policies, encourage and support enterprises to introduce a number of innovative research teams and leaders who have mastered key and core technologies in a planned, step-by-step and targeted manner. Talents, constantly improve the visibility and influence of China's LED industry circle. Give play to the role of higher education institutions and scientific research institutions in cultivating high-level talents, further optimize the structure of higher education, personnel training system and training direction, encourage qualified universities to set up LED industry majors, and give priority to enrollment planning and professional construction funding. stand by. Encourage school-enterprise cooperation and explore new directions for jointly training innovative talents in strategic emerging industries. Accelerate the cultivation of cutting-edge talents that are urgently needed at this stage, and at the same time increase the training of reserve talents, break through the bottleneck of talents, overcome technical barriers, promote the seamless connection between the talent chain and the industrial chain, and enhance the independent innovation and industrial competitiveness of China's LED industry.

Edit; Nizi

Uv Air Sterilizer,Uv Light Air Sterilizer,Medical Device Sterilization,Mobile Type Uv Air Sterilizer

Dongguan V1 Environmental Technology Co., Ltd. , https://www.v1airpurifier.com